Monthly Economy & Travel Industry Summary: August 2025

Weak jobs report raises odds of rate cut, while international travel by Americans continues to rise

At a glance: Weak jobs report raises odds of September rate cut

- The economy is growing below its potential, but a recession this year remains unlikely.

- Wage growth is outpacing inflation, and spending will receive further support in 2026 from tax breaks and refunds in the One Big Beautiful Bill Act.

- The weak labor report for July, combined with recent comments by the Chair of the Federal Reserve, makes a September rate cut likely.

The Details

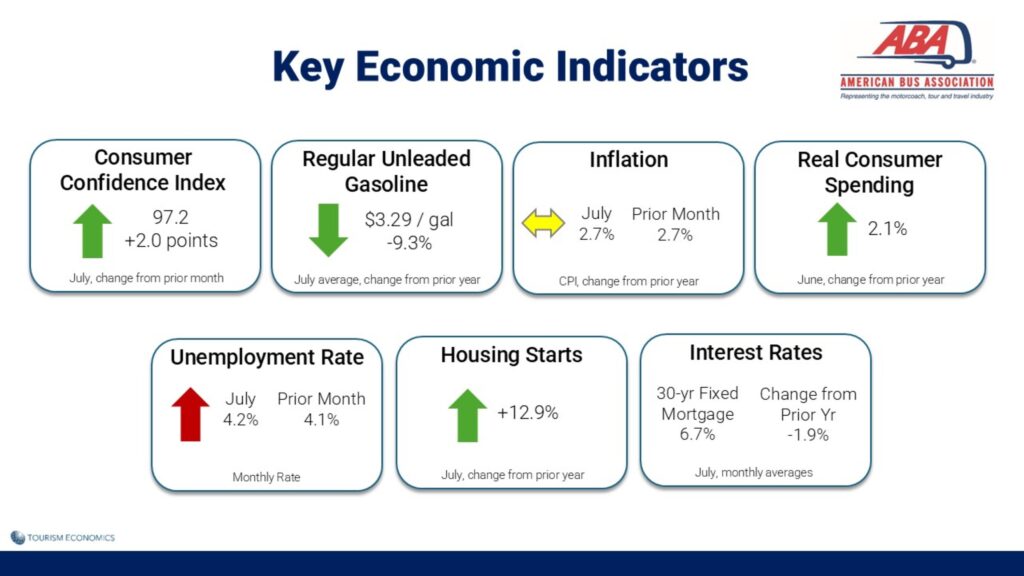

The health of the US economy is being questioned due to the downward revisions in the July employment report. While the revisions suggest the labor market is weaker than assumed, they didn’t alter our assessment of the broader economy. In our August update, we raised our US GDP growth forecast for 2025 by 0.1ppt to 1.7% and lowered it by the same magnitude to 2% for 2026 based on a better understanding of what was included in the One Big Beautiful Bill Act.

The economy has clearly slowed from the robust growth displayed over the prior two years, and the Conference Board’s leading economic index (LEI) has steadily declined throughout 2025. However, we are suspect of the impending recession signaled by the LEI’s six-month growth rate. Declines in the index remain concentrated in the less reliable soft data, and the LEI can send false signals, as it did for much of 2023 and 2024.

This doesn’t mean the economy isn’t vulnerable. Hiring has slowed, the housing market is in recession, and price pressures are rising, while policy uncertainty is weighing on job growth and non-IT-related business investment in equipment and structures.

On the other hand, layoffs remain low, hard data from the manufacturing sector has improved, AI and data centers are providing a boost, and measures of uncertainty are improving. Looking ahead, the economy is expected to receive a boost from fiscal policy, lower interest rates, and reduced uncertainty in 2026.

July’s surprisingly weak jobs report increased the pressure on the Federal Reserve to cut rates sooner rather than later. Following Fed Chair Jerome Powell’s speech at the annual international conference hosted by the Federal Reserve Bank of Kansas City in Jackson Hole, Wyoming, we have moved up our expectation for the next rate cut from December to September.

The gain of 73,000 payroll jobs in July was only slightly below expectations, but the downward revisions for the previous two months are what caught the eye of rate-cutting advocates. The result is that the economy generated only 35,000 jobs per month from May through July, the slowest three-month pace since June 2020, when the economy was just emerging from the pandemic recession. Before that, you have to go back to 2010 to find a weaker stretch of job growth.

The slowdown in hiring would be considerably deeper if not for job gains in the health and social services sector. Indeed, take out the job gains in this mostly noncyclical sector that reflects an aging population, and private sector job growth would show a decline over the past three months. Moreover, manufacturing jobs, which tariffs are designed to bolster, fell for the third consecutive month in July, a stretch of losses not seen since the pandemic.

The downward revisions to payrolls in previous months align with the sluggishness in consumer spending over the first half of the year. From the beginning of the year through June, real personal consumption was virtually flat, notching a small 0.1 percent decline. Such a lengthy period of stagnant spending is rare outside of a recession and has not occurred since the six months encompassing the 2020 pandemic. Before that, the previous episode took place during the tail-end of the 2007-2009 Great Recession.

That said, there are reasons to believe that consumers are not about to zip up their wallets going forward. Average hourly earnings rose at an annual rate of 3.9 percent in July, comfortably outpacing the increase in inflation and supporting the purchasing power of jobholders. Additionally, households will be getting tax breaks and refunds in 2026 that should pad their bank accounts, even as other fiscal measures will incentivize employers to keep hiring and spending.

Revisions to prior months in the July labor report generated worries about the validity of the data, but revisions are a feature, not a bug, of employment data. Inherently, there is a trade-off between timeliness and accuracy. The initial estimate of employment is revised in each of the subsequent two months and then is adjusted as part of the annual benchmark process.

Revisions in subsequent months partly occur as additional responses become available. The response rates for the second and third estimates of nonfarm employment are significantly higher than the initial. Historically, small businesses and governments are among those with a tendency to report late.

While the recent revisions appear large at face value, they aren’t. The difference between the current estimates of employment minus the initial estimate as a share of the initial estimate has been small and has trended lower over time. In short, revisions show that the BLS is incorporating new information, as it has always done, and is attempting to get it correct.

At a glance: International travel by Americans continues to rise

- Hotel demand and airport passenger volumes are stagnating.

- Luxury hotels are experiencing the strongest growth, and growing outbound travel by US citizens suggests travel is being supported by higher-income households.

- Depreciation of the US dollar may lend some support to the domestic travel industry.

The Details

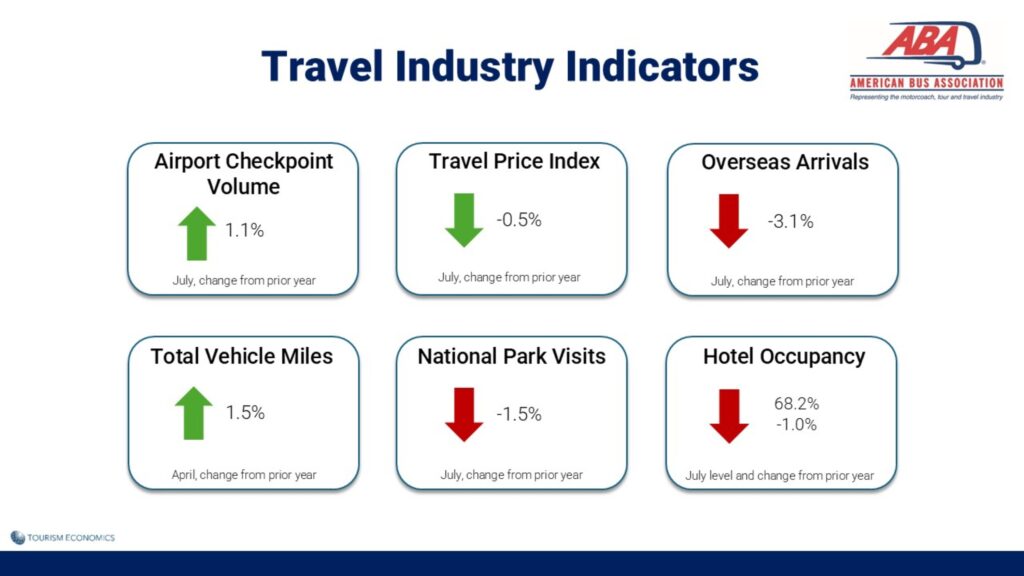

The travel sector has experienced little growth in 2025. Hotel demand was up just 0.1% year-to-date through July, and the number of people passing through TSA checkpoints in US airports was down 0.4% through the first seven months of the year.

The stagnant growth in hotel demand and airport volume aligns with consumer spending, which was essentially flat (-0.1%) over the first half of the year. Taken together, these results suggest consumers have adopted a wait-and-see mentality amid heightened uncertainty due to tariffs and a slowdown in hiring.

The weak performance prompted a slight downgrade to the hotel forecasts released in August by STR and Tourism Economics, with the forecast of hotel demand growth in 2025 reduced from 0.5% to -0.1%. After taking into account growth in the supply of hotel rooms, the average occupancy rate is projected to decline 1% this year.

Not all segments of the travel industry are experiencing the same weakness. Luxury hotels have experienced the strongest demand growth this year, while economy hotels have seen the largest decline in demand.

Outbound travel is also outperforming the overall industry. Through May, the number of international trips by US residents was 5.0% higher than the same period last year. Travel to Mexico was up 7.7%, and overseas travel was up 4.7%. Conversely, US resident travel to Canada was down 4.7% through May.

Meanwhile, inbound travel continues to weaken in 2025. Overseas arrivals (excluding Canada and Mexico) declined 3.1% in July, marking the third consecutive month of declines and bringing year-to-date overseas arrivals 1.6% below the same period in 2024. In total, overseas arrivals have declined by 304,000 through July compared to the same period last year, with losses from Western Europe (164,000) and Asia (136,000) accounting for the majority of the decline.

In percentage terms, the sharpest year-to-date declines have come from Africa (-6.0%) and Oceania (-3.3%). Arrivals from Western Europe are down 2.3% so far this year, including steep declines from Germany (-10.1%) and Switzerland (-7.6%).

International declines are likely to continue through the fall. Air bookings for international inbound travel continue to trail prior year levels, currently running 10% to 14% below this time last year for travel from August through October.

The largest declines, by far, have been from Canada. Land arrivals from Canada to the US declined 37.0% in July, extending a downward trend that began in February. Air arrivals also continued to weaken, down 25.8% in July. Through July, total arrivals from Canada have decreased by 25.2% compared to the first seven months of 2024.

Meanwhile, interest in trips from Canada to Mexico is strong, with air bookings for trips during August to October running 12% to 13% ahead of levels at the same point a year ago.

The sharp decline in travel to the US from Canada is placing particular pressure on states along the Canadian border. Most US states bordering Canada have experienced larger year-to-date declines in hotel demand than the national average. For example, hotel demand in Maine was down 5.3% year-to-date, versus +0.1% nationally.

Depreciation of the US dollar could help narrow the imbalance between growth in outbound travel and declining inbound arrivals by making international travel more expensive for US residents and more affordable for international visitors. The dollar has stabilized recently after weakening earlier this year, and we anticipate the US dollar will depreciate further next year. Headwinds for the dollar include a less positive growth outlook for the US economy relative to the rest of the world and narrowing interest rate differentials as the Fed cuts aggressively next year. US fiscal sustainability concerns and ongoing repositioning of international portfolios will also put downward pressure on the dollar.

The Monthly Economy & Travel Industry Summary partners with Tourism Economics, an Oxford Economics company. Combining rigorous economic analysis with decades of travel industry expertise, Tourism Economics is an industry-leading insight resource. Learn more at www.tourismeconomics.com.